Payment automation saves lives.

Okay, not really — but online payment software definitely saves time.

According to a PWC report, finance teams spend 30% of their time collecting data and reconciling it between systems. What if they didn’t have to?

Keep reading to learn everything you need to know about payment automation before investing in it, including how it works, whether it's secure, and what you can expect when you make your payment processing an automated process instead.

Sign up for a Free Trial today.

SHORTCUTS

What is payment automation?

Payment automation is any invoicing and payments software that integrates with your accounting software. Through payment automation, customers can pay businesses and receive payments by credit card, Electronic Funds Transfer payments (EFT), Automated Clearing House payments (ACH), e-transfers, etc., in multiple currencies.

How does payment automation work?

Payment automation works by using software, cloud computing, and digital payment encryption to centralize invoice and payment processing in a secure place. Then, through API integration, payments software and accounting software can share data through the cloud, eliminating manual double-entry accounting through real-time financial reporting. A payment automation solution helps businesses replace their manual payment processing.

Why is payment automation important?

Payment automation is important for saving time and reducing data errors. When payment processing is automated, finance teams no longer need to send paper invoices, process paper checks, and enter data manually in financial reports — all steps that introduce the possibility for human error. Payment automation systems can minimize errors like duplicate payments or incorrect payment amounts.

Automating your payment processes is now known to save finance teams 20–40 hours per week, as well as facilitating cost savings by switching to digital processes.

How to start automating payments

You’ll need to invest some time upfront in payment automation, but you’ll get that time back soon after you send your first electronic invoice. Here we’ll walk you through the steps to start automating payments:

1. Conduct an audit of your financial documents.

Your online payment software is only as good as the data you feed it. Make sure your data is clean by taking stock of your financial statements, customer and vendor contracts (including credit and payment terms), and outstanding payments. You’ll input information from these documents into your payment and accounting software later.

2. Get accounting software like Quickbooks or Xero.

To get the most of your automated payment system, you'll need accounting software like Quickbooks or Xero to handle holistic financial reporting. You can try a few options for free before choosing one that works for your business.

3. Create your customer contact cards.

After you choose and set up your software, you’ll need to create your customer contacts. A contact card contains information like the customer’s legal business name, billing address, mailing address, currency, payment terms, and payment method.

4. Get invoice and payment processing software like Plooto.

Choose online payment software that integrates with your accounting software. When you do, you'll be able to offer your customers multiple payment options like credit card, EFT payments, ACH payments, e-transfers, etc. If your customers are in more than one country, choose software that lets you accept payments in multiple currencies.

5. Connect your payment software to your accounting software.

Software integrations are where you’ll save time and reduce errors in your financial reporting. Make sure your accounting software shares data with your payments software, and vice versa. When you want to reconcile data between your payments and your financial reports, you won’t need to do it through manual double-entry accounting.

6. Optional: Set up pre-authorized debit (PAD) agreements for recurring payments.

You don't need this step for your payment automation system, but you may want to consider it if you have many recurring payments from customers. A PAD agreement authorizes secure automatic payments from a customer's bank account moving forward and allows for a payment schedule. When a payment is made, the information will sync back to your accounting software.

7. Send electronic invoices with automated reminders and messages.

Congrats — you’re ready to send your first invoice! It should include your contact information, the company’s contact information, the balance due, payment terms, balance due dates, and line items describing products and services rendered. Online payment software also allows you to pre-populate reminders with personalized messages in the event a payment is late — so you won’t need to remember to chase down your money. Consider adding the option for early payment discounts to encourage prompt payment.

8. Use auto-reconciliation to sync your financial data.

A last step before you start receiving payments: Make sure the data from your payment processing software is populating your accounting software. Once this is working properly, you can safely stop the manual double-entry accounting and focus on other areas of your business.

How payment automation solves common accounting problems

- Manual vs. automated accounts payable processes

- Lack of visibility into spending

- Simplifying digital payments

- Making payments more flexible

Now that you know how to evaluate online payment software, we’ll get into the details of what you should expect — maybe even demand — for your automated payment system.

When you invest in payment automation, you should see clear “before” and “after” scenarios, felt immediately in your accounts payable department. If you don’t, it’s time to seek another online payment option.

But what does a good before-and-after look like? Here are some of the most common problems a good payment automation process addresses:

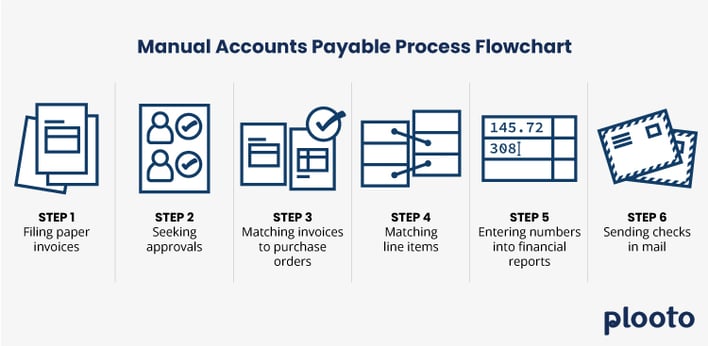

Manual vs. automated accounts payable process

When your accounts payable process is manual, it looks something like this:

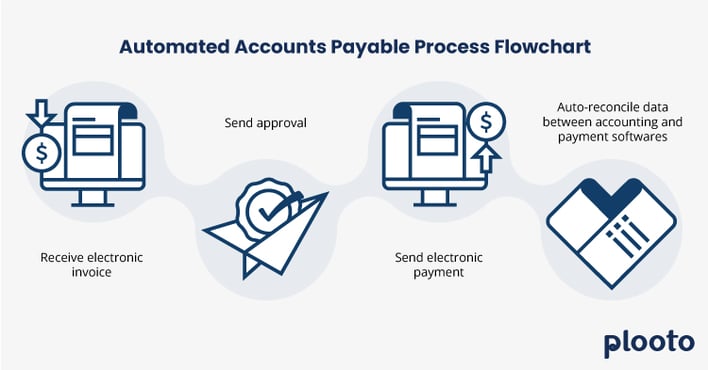

But when you automate the accounts payable process, you’re eliminating many of these steps. Instead the process should look something like this:

Lack of visibility into spending

Effective accounts payable and accounts receivable processes lead to accurate cash flow statements. Cash flow statements are crucial for running your business.

Cash flow statements track incoming and outgoing money. When your head of finance asks how much money is about to come in and go out, they want “visibility of spend”, which is what your cash flow statement serves to do.

When you know you have money set to come in — accounts receivables — you can count this as revenue you can spend to grow your business. On the flip side, when you know you have a ton of accounts payables going out — or, maybe a lot of bad debt — you’ll know it’s time to pull back on the expenses for a bit.

But see, you can’t know any of this if your financial reports aren’t updated in real-time. As we mentioned above, manual processes introduce too many possibilities for error and delay. The solution is simple:

Make or receive electronic payment → Auto-reconcile data with accounting software → See updated data in financial reporting

Simplifying digital payments

We’re not going to lie to you — accepting digital payments through credit card, EFT, ACH, e-transfers, etc. can be daunting. You’ll be making your life easier for your customers, but tracking multiple payment channels isn’t a walk in the park.

This is why centralization matters, which is what automated payments offer. When you use one payment platform to track invoicing, payment status, and all types of digital payments, your payment related data lives in one place — never lost, never hunted for, always accurate.

Making payments more flexible

Customers love flexible payments — and limitations on payment options can actually hurt your business.

If you only accept checks or credit cards but your customer wants to pay you via wire transfer, what should you do? Good customer service means allowing the customer to choose how they want to pay. If you don’t, the customer could be spinning their wheels trying to figure out how to pay you, and you could end up with a late payment (or no payment at all).

Online payment software that works for your business expands your options. Huge bonus if they also allow you to expand internationally by allowing you to collect payments in multiple currencies.

How to evaluate payment automation software

Before settling on payment automation software for your business, you’ll want to evaluate several options:

Frequently asked questions about online payment software

Will payment automation provide access to financial data?

When you implement payment automation, your financial data exists in the cloud. Through API integrations, your accounting software and payment software share data — meaning it’s the same across both channels. Online payment software gives you better access to your financial reporting through real-time, accurate data, which makes it easier to share it with other members of your team.

Does payment automation work with existing systems?

Yes, payment automation works with existing accounting software. Online payment software only handles accounts receivable and accounts payable processes, which is a lot but it’s only one small piece of accounting.

Robust accounting systems like Quickbooks and Xero work with payment software through API integrations that allow two pieces of software to share data with each other — meaning financial data in one exists in the other with auto-reconciliation. That means your holistic accounting processes and reporting may still be handled with accounting software, but with the aid of payment software.

Is payment automation safe?

Yes, payment automation is safe and secure. Data encryption and tokenization are technological marvels that have advanced streamlined digital payments around the world.

Tokenization is used to secure data for electronic payments. Tokenization keeps bank details, credit card information, and customer information safe and encrypted during transactions. When a payment is made, a token is created to signal to financial institutions that the payment is valid. This happens during credit card transactions, debit transactions, refunds, recurring payments, etc.

Payment automation software also requires two-factor authentication upon login, which means your access is attached to your smartphone — an added layer of security commonly used by governments and banks.

How much does it cost to automate payments?

Payment automation isn’t expensive. There are two components to payment automation: what you pay for the software, and what you pay in processing fees.

You can purchase great online payment software for $25 per month. Most providers give you access to a 30-day free trial so you can try the software before purchasing it. If you want to start making international payments, some providers offer a flat monthly fee for the service.

Automate payments with Plooto

Plooto helps businesses manage their invoices and payments from a centralized place. With accounting software integrations, Plooto’s auto-reconciliation feature keeps your financial records up to date — when you get paid, your books are updated automatically, making the whole thing a streamlined process.

Some of Plooto’s top features include:

- Next-day vendor payment

- Payment receipt within two days

- Secure ACH/EFT payments, credit card payment, and wire transfers

- Accounting integrations with Quickbooks and Xero

- ISO 27001 standard certification

- Insurance policies

- International payments across 30+ countries

Getting paid on time is easier when you’re using Plooto’s automated reminders to communicate with customers. When Plooto customers combine the time they’re saving on reconciling their books with the time it usually takes to follow up with customers on payment, they’re saving between 20-40 hours per week.

Sign up for a Free Trial today

CHAPTERS

00 Considering Online Payment Software? Payment automation explained

01 Accounts payable software: A guide for strategies, benefits, and solutions

02 Accounts receivable software: A guide for strategies, benefits, and solutions

03 What is the future of Accounts Payable?

04 Comparing the best AR automation software solutions

05 What’s the best AP software for your business? 5 Top vendors compared

06 Scaling for growth with AP automation